Average 30-Year Fixed-Rate Mortgage at 6.22%

March 19, 2026

The 30-year fixed-rate mortgage edged up this week to 6.22% but remains nearly half a percentage point lower than the same time last year. Potential homebuyers are poised for a more affordable spring homebuying season than last with the market experiencing improvements in purchase applications and pending home sales.

- The 30-year fixed-rate mortgage averaged 6.22% as of March 19, 2026, up from last week when it averaged 6.11%. A year ago at this time, the 30-year FRM averaged 6.67%.

- The 15-year fixed-rate mortgage averaged 5.54%, up from last week when it averaged 5.50%. A year ago at this time, the 15-year FRM averaged 5.83%.

Information provided by Freddie Mac.

Existing Home Sales

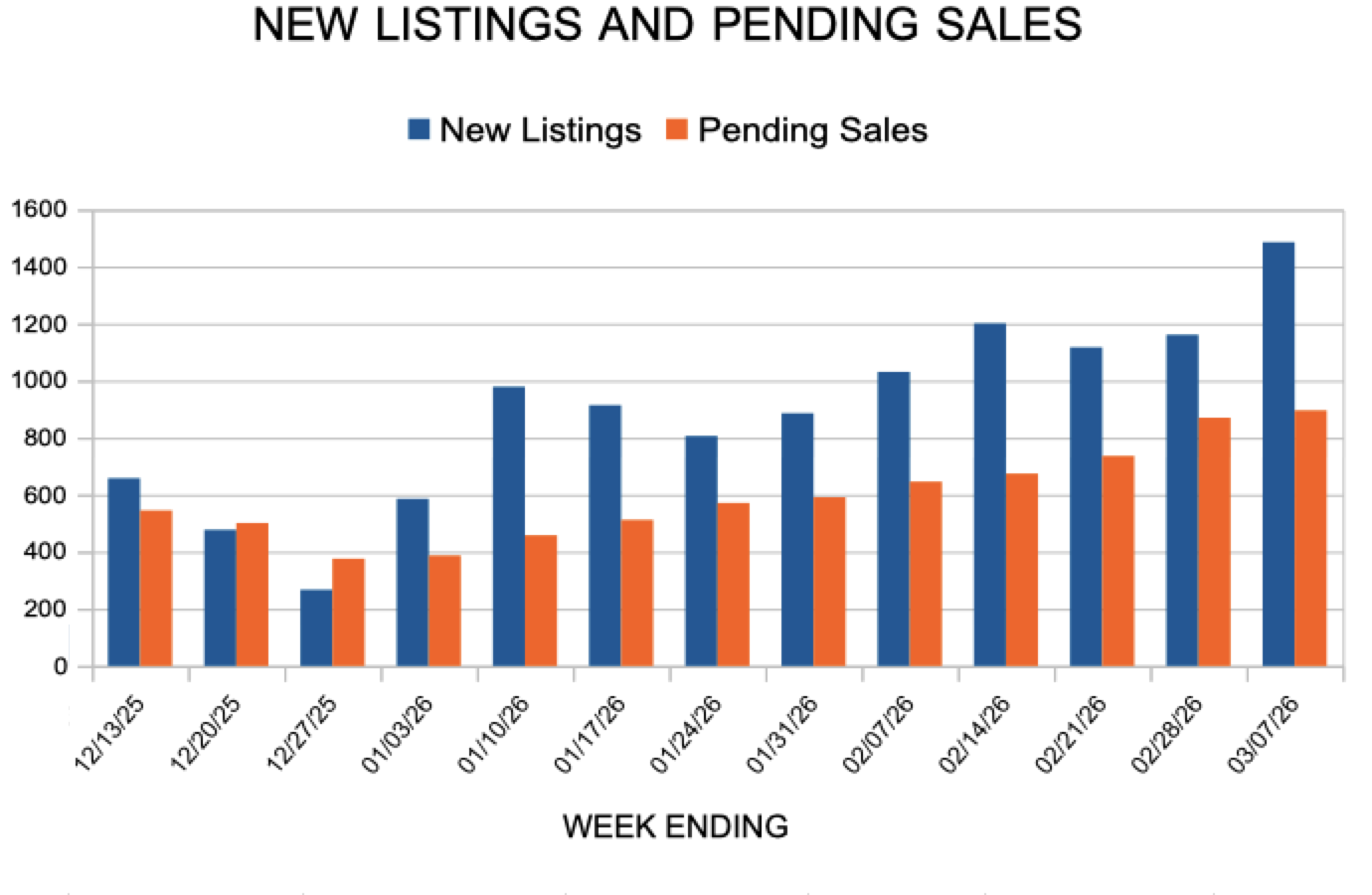

New Listings and Pending Sales

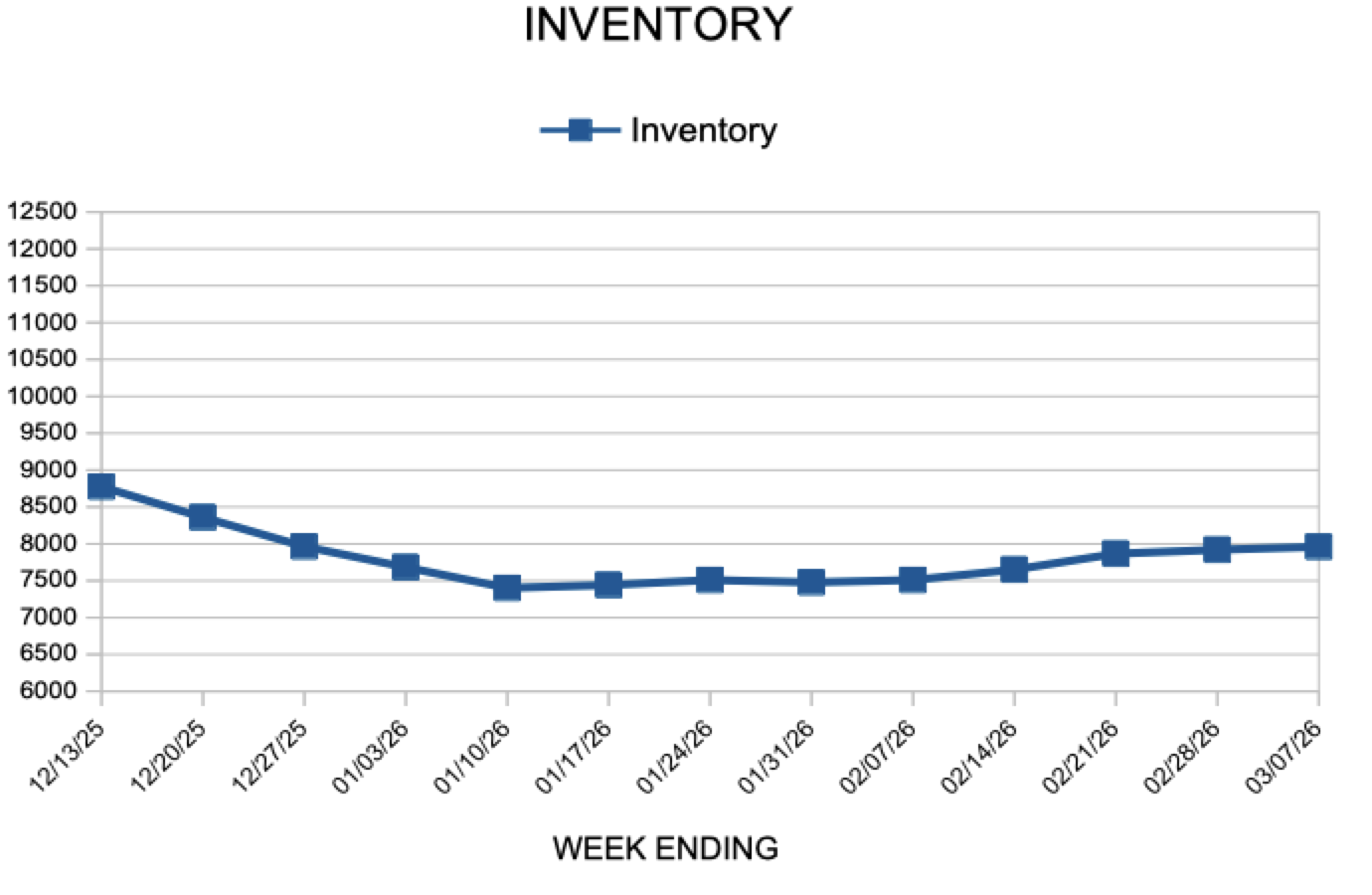

Inventory

Weekly Market Report

For Week Ending March 7, 2026

U.S. sales of new residential homes slipped 1.7% in December to a seasonally adjusted annual rate of 745,000, according to the U.S. Census Bureau. Despite the monthly decline, new-home sales were 3.8% higher compared with the same period one year earlier. There were an estimated 472,000 new homes for sale, representing a 7.6-month supply at the current sales pace.

In the Twin Cities region, for the week ending March 7:

- New Listings increased at 1,486

- Pending Sales increased 1.7% to 896

- Inventory increased 3.1% to 7,959

For the month of February:

- Median Sales Price remained flat at $380,000

- Days on Market remained flat at 69

- Percent of Original List Price Received decreased 0.3% to 97.4%

- Months Supply of Homes For Sale remained flat at 2.1

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.